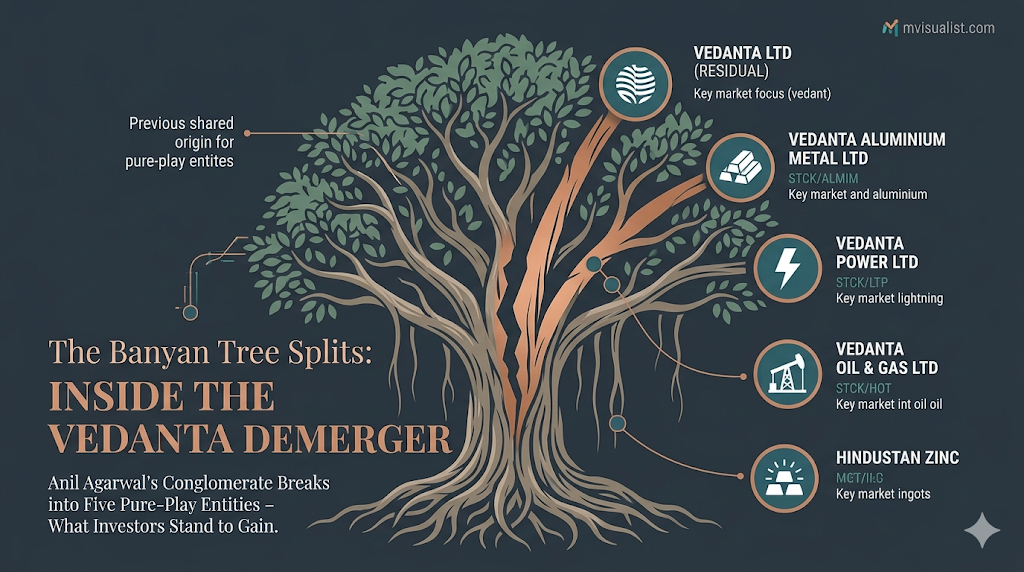

The Banyan Tree Splits:

Inside India’s Most Ambitious Demerger

Anil Agarwal’s Vedanta has shattered its conglomerate mould — breaking into five pure-play listed entities. We unpack what happened, why it matters, and what investors stand to gain.

There is a metaphor Anil Agarwal once used to describe his sprawling empire. “Vedanta is like a big banyan tree,” he told PTI in late 2025. “There is tremendous potential in each business, and each one of them has the potential to become a banyan tree by itself.”

Those words were not just poetic — they turned out to be prophetic. On May 1, 2026, the record date for one of the most consequential corporate restructurings in Indian market history quietly passed. Vedanta Limited, the metals-and-mining giant listed on the NSE and BSE, officially ceased to exist in its original conglomerate form. In its place, five leaner, sharper, sector-focused entities emerged from the trunk.

For the company’s over two million shareholders, the implications are profound. For India’s capital markets, the reverberations are only just beginning.

A Plan Three Years in the Making

The idea of breaking up Vedanta had been brewing for years inside the boardrooms of Vedanta Resources — the London-headquartered parent controlled by Agarwal’s Volcan Investments (since renamed Vedanta Incorporated). The logic was straightforward, even if the execution was anything but: Vedanta had long traded at a conglomerate discount, a well-documented market phenomenon where investors apply lower valuation multiples to diverse, non-synergistic assets bundled under a single roof. A zinc mine, an oil field, an aluminium smelter, and a power plant share almost nothing in common — yet Vedanta’s single stock price forced the market to price them all as one.

Initial announcement. Volcan Investments / Vedanta Resources proposes demerging the conglomerate into six independent listed entities, initially including a separate semiconductor and display vertical.

Overwhelming approval. Shareholders vote 99.99% in favour; secured creditors 99.59% and unsecured creditors 99.95%. The plan is revised to five entities for tighter operational clarity.

NCLT gives the green light. The National Company Law Tribunal approves the composite scheme of arrangement. Shares rally nearly 4%. A certified copy of the order is received January 31, 2026.

Ex-demerger date. Vedanta shares open at ₹289.50, settle around ₹271.50 after falling ~7%. The drop is a technical accounting adjustment, not a destruction of investor wealth.

Record date. Demerger becomes effective. Shareholders receive entitlement to one share each in four new entities. All four shares sit frozen in demat accounts pending exchange listing approval.

Listings begin. Vedanta files with stock exchanges for listing approval this week. All four new entities expected to commence independent trading — aligning with CFO Ajay Goel’s Q1 FY2027 target.

The Five Entities — What You Now Own

Under the composite scheme, every Vedanta shareholder receives one share in each of the four newly carved-out companies for every one Vedanta share held on the record date. The residual Vedanta Limited continues as the fifth entity. A single Vedanta shareholder now has exposure across five distinct, independently listed companies.

Retains Hindustan Zinc, Zinc International, copper, ferro chrome, nickel, and new-age semiconductor and display ventures. The most stable cash generator — yield-oriented, anchored by zinc’s infrastructure demand and Hindustan Zinc’s silver contribution.

The analysts’ unanimous favourite. India’s largest aluminium producer. Bharat Aluminium (Balco) transfers into VAML as part of the reorganisation. Contributed approx. ₹15,909 Cr to revenue in FY25. ICICI Direct targets listing valuation of over ₹400/share.

Talwandi Sabo Power Limited is renamed Vedanta Power. Houses the group’s energy generation assets — thermal and growing renewable capacity. Ranked among the more attractive units by ICICI Direct alongside aluminium.

Malco Energy Limited, renamed as Vedanta Oil & Gas, consolidates upstream exploration and production operations. Carries strategic importance given India’s energy security priorities, though performance remains sensitive to global crude price cycles.

Houses iron ore and steel operations with sharper visibility as a standalone entity. Positioned to capitalise on India’s infrastructure-led ferrous metal demand, though exposed to commodity cycles and legacy regulatory risk in mining operations.

Why Break Up at All? The Case for Demerger

Vedanta’s management outlined four core problems the restructuring aimed to solve — problems universal to large diversified conglomerates but felt acutely in a capital market that increasingly rewards focus and transparency.

1. The Conglomerate Discount

Capital markets have long penalised companies that bundle unrelated businesses. Investors who want aluminium exposure do not want to simultaneously buy oil & gas risk. The result: Vedanta’s stock consistently traded below the sum of its parts. The demerger forces the market to price each vertical on its own merits — potentially unlocking substantial latent value for shareholders.

2. Restricted Capital Access

As a single entity, Vedanta’s perceived debt burden made equity capital markets relatively difficult to access. Five separate entities, each with their own balance sheet and growth story, open far more avenues for raising sector-specific capital independently — without one vertical’s debt dragging another’s cost of capital upward.

3. Investor Universe Mismatch

A fund focused on energy could not cleanly buy Vedanta without also taking on aluminium and zinc exposure. Post-demerger, Vedanta Aluminium Metal attracts metals-sector specialists; Vedanta Oil & Gas speaks to energy investors. A broader, more targeted investor base should, over time, compress valuation discounts further.

4. Centralised Management Distortion

When every vertical competes for the same management attention and capital allocation budget, sub-optimal decisions accumulate. Independent boards, management teams, and P&Ls for each entity eliminate these internal distortions — allowing each business to pursue niche strategies and attract the right talent.

“Vedanta is like a big banyan tree. There is tremendous potential in each business, and each one of them has the potential to become a banyan tree by itself.”

— Anil Agarwal, Chairman, Vedanta Resources, December 2025What This Means for 2 Million Shareholders

For retail investors, the demerger mechanics are simple in principle but worth understanding precisely — because misinformation about the share price drop caused considerable confusion around the ex-date.

The 1:1 ratio. For every 1 Vedanta share held on the record date (May 1, 2026), shareholders receive 1 share each in Vedanta Aluminium Metal, Vedanta Power, Vedanta Oil & Gas, and Vedanta Iron & Steel. They also continue holding original Vedanta shares in the residual entity. A single pre-demerger Vedanta share thus becomes five distinct holdings.

The April 30 price drop. Vedanta shares fell sharply on the ex-demerger date — from a previous close of ₹773.60, settling around ₹271.50. This was not a loss. It was an accounting adjustment reflecting the value of four businesses being separated out. The combined market capitalisation of all five entities should approximate the original single-entity value.

The frozen shares. The four new entities’ shares currently sit frozen in demat accounts. No trading is permitted until stock exchanges approve their listing — an event expected by mid-June 2026, within CFO Ajay Goel’s stated Q1 FY2027 target.

The T+1 rule. Investors who purchased Vedanta on May 1 itself did not qualify. Under India’s T+1 settlement cycle, eligibility required shares to be in the demat account by April 30, 2026.

What the Street Is Saying

Analysts Shashank Kanodia and Manisha Kesari see Vedanta Aluminium Metal as the standout, with a listing valuation expectation exceeding ₹400/share. They note favourable global supply dynamics, elevated aluminium prices, and ongoing capacity expansions. “Investors should hold the stock and play the demerger, as they stand to gain post listing of all entities.” Vedanta Power is also ranked highly.

Head of Fundamental Research Sunny Agrawal highlights the Zinc business as the residual entity’s core strength — with industry-leading cost of production and an increasing silver revenue contribution from Hindustan Zinc. The zinc thesis: high cost efficiency, steady infrastructure demand, and a consistent dividend pipeline from Hindustan Zinc.

Chief Research Officer Ravi Singh notes the restructuring improves transparency and capital allocation, with zinc, copper, and aluminium identified as highest-quality segments. He flags persistent risks: elevated debt at Vedanta Resources and broad commodity cycle sensitivity. Dividend visibility may also evolve materially post-demerger as each board sets independent payout policies.

Risks Investors Cannot Ignore

| Risk Factor | Description | Severity |

|---|---|---|

| Parent Debt Overhang | Vedanta Resources (the London parent) carries significant external debt. Dividends from listed Indian entities remain the primary repayment mechanism — potentially constraining capex freedom at the entity level. | High |

| Commodity Cycle Sensitivity | All five entities operate in cyclical commodity markets. A broad downturn in aluminium, zinc, or crude prices can simultaneously compress margins across the entire group portfolio. | High |

| Listing Price Discovery | Until the four new entities begin trading, true market valuations remain theoretical. Initial sessions may see significant volatility as institutional and retail price discovery occurs simultaneously. | Medium |

| Regulatory & Mining Risk | Iron ore mining and copper smelting operations have historically faced regulatory scrutiny in India. VISL and the copper vertical carry this legacy regulatory overhang. | Medium |

| Mutual Fund Rebalancing Pressure | Funds holding Vedanta that have sector-specific mandates may be compelled to sell newly allocated shares outside their investment scope — creating short-term selling pressure post-listing. | Medium |

| Dividend Policy Uncertainty | How each entity approaches dividend distribution independently remains unclear. Some may prioritise growth capex over payouts, affecting income-focused investors who held Vedanta for its dividend yield. | Low–Med |

A Template for Indian Conglomerates?

Vedanta’s demerger does not exist in isolation. It follows a global trend of large industrials rethinking the conglomerate model — from GE’s historic three-way split to Johnson & Johnson’s consumer health spinoff. In India, the question is increasingly relevant for other sprawling groups navigating similar conglomerate discount dynamics.

What makes Vedanta’s restructuring particularly significant is the sheer scale and speed. From first announcement to effective demerger date: under three years. From NCLT approval to record date: under five months. The near-unanimous shareholder vote — 99.99% in favour — reflects not just institutional conviction but a broader recognition that focused companies, over time, tend to outperform diversified ones in capital markets.

Post-demerger, each Vedanta entity must now stand on its own: its own management, its own strategy, its own investor narrative. The aluminium business cannot hide behind zinc’s cash flows. The oil & gas unit cannot lean on aluminium’s EBITDA margin. Good performance in one business will no longer mask underperformance in another.

That is, ultimately, the point. Accountability. Transparency. And the freedom to grow at the speed each business deserves.

The Bottom Line

The Vedanta demerger is one of the largest and most complex corporate restructurings in Indian capital market history. Effective from May 1, 2026, it creates five independent listed entities — each with its own sector focus, capital structure, and investor proposition. For shareholders who held Vedanta through the record date, the portfolio has effectively multiplied into five distinct stock positions. The coming weeks — as all four new entities seek listing and begin trading on the NSE and BSE — will be the true test of whether the sum of the five parts exceeds the value of the single whole that once was Vedanta.

All four new companies are expected to begin independent trading by mid-June 2026, subject to stock exchange approval.