25 Finance Terms

You Must Know

Before Investing

Every expert investor started exactly where you are now — unfamiliar with the jargon. This glossary strips the complexity out of the vocabulary so you can walk into any investment conversation with clarity and confidence.

The financial world speaks a language of its own — a dense shorthand built up over centuries of markets, crises, and innovation. For a first-time investor, walking into that world without a vocabulary can feel like travelling to a foreign country without a phrasebook. You know something important is being said; you just can’t quite follow it.

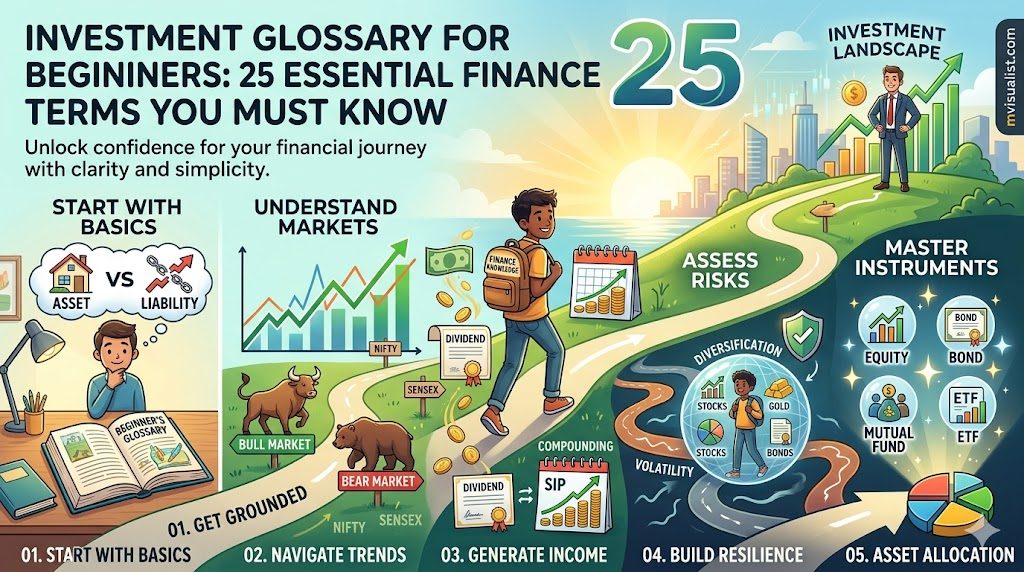

This guide is that phrasebook. We have grouped the 25 most essential finance and investing terms into five categories — Basics, Markets, Returns, Risk, and Instruments — each explained in plain language with a real-world example to anchor the definition.

Category 01 — The Basics

Anything you own that has monetary value and can generate future economic benefit. Assets are the building blocks of any investment portfolio — you are essentially choosing which assets to own.

The opposite of an asset — a financial obligation or debt you owe to someone else. Understanding the difference between assets and liabilities is the foundational insight of personal finance: build assets, minimise liabilities.

Wealth in the form of money or assets that is deployed to generate more wealth. Capital is the fuel of investment — you put it to work by purchasing assets that you expect to appreciate or generate income.

The complete collection of all investments held by an individual or institution at any given time. A portfolio can contain stocks, bonds, mutual funds, real estate, gold — anything. The composition of your portfolio determines your risk and return profile.

Often called the eighth wonder of the world, compounding is the process by which returns on an investment are reinvested to generate their own returns over time. The longer your investment horizon, the more dramatic the compounding effect becomes — which is why starting early is one of the most powerful things a new investor can do.

The investor who understands compounding does not ask “how much can I make?” They ask “how long can I stay invested?”

mvisualist editorialCategory 02 — Markets

A market condition characterised by rising prices and widespread investor optimism. Technically, a bull market is declared when prices rise 20% or more from a recent low. Bull markets can last months or years and are driven by strong economic fundamentals, corporate earnings growth, and positive sentiment.

The opposite of a bull market — a period of falling prices (typically a 20%+ decline from recent highs) and pervasive pessimism. Bear markets test investor conviction. Historically, every bear market has been followed by recovery, which is why staying invested matters.

The total market value of all outstanding shares of a publicly listed company. Market cap = Share price × Total number of shares. It is the most common measure of a company’s size and is used to classify stocks as large-cap, mid-cap, or small-cap.

A benchmark that tracks the collective performance of a selected group of stocks. An index does not buy stocks — it measures them. Indices are used to gauge overall market direction and serve as the yardstick against which fund managers are measured.

How quickly and easily an asset can be converted into cash without significantly affecting its price. High liquidity is generally desirable — it means you can exit your investment when needed. Low liquidity can trap you in a position at the wrong time.

The first time a privately held company offers its shares to the general public on a stock exchange. An IPO allows the company to raise capital from public investors while giving those investors an opportunity to own a stake in the business.

Category 03 — Returns

Compound Annual Growth Rate. The smoothed annual growth rate of an investment over a given period, assuming profits are reinvested each year. CAGR is the single most useful metric for comparing investment performance over different time horizons.

A portion of a company’s profits distributed to shareholders, typically paid quarterly or annually. Dividends are one of two ways shareholders earn returns (the other being capital appreciation). Not all companies pay dividends — growth-stage companies often reinvest profits instead.

The increase in the market value of an asset over time. When the price of a stock, property, or mutual fund unit rises above what you paid for it, the difference is your capital appreciation — also called capital gain when you actually sell.

The per-unit price of a mutual fund scheme, calculated daily by dividing the total value of the fund’s assets minus liabilities by the number of outstanding units. NAV is to mutual funds what share price is to stocks.

A method of investing a fixed amount into a mutual fund at regular intervals — monthly, weekly, or quarterly — rather than as a lump sum. SIPs harness the power of rupee cost averaging: you buy more units when prices are low and fewer when prices are high, which smooths out your average cost over time. For most retail investors, a SIP is the most practical and disciplined way to build wealth.

A SIP is not just an investment tool. It is a financial habit that removes emotion from the equation — the single biggest edge a retail investor can have.

mvisualist editorialCategory 04 — Risk

The degree to which an investment’s price fluctuates over time. High volatility means large price swings — up or down. Volatility is not inherently bad; it creates both opportunity and risk. For long-term investors, short-term volatility is noise. For short-term traders, it is the game.

The practice of spreading investments across different asset classes, sectors, geographies, or instruments to reduce the impact of any single investment’s poor performance on your overall portfolio. Simply put: don’t put all your eggs in one basket.

The level of risk an investor is willing and able to accept in pursuit of their financial goals. Risk appetite is shaped by age, income stability, financial goals, and psychological comfort. Knowing your own risk appetite is the first step to building an appropriate investment strategy.

The risk that the return on your investment will not outpace inflation, causing your money to lose real purchasing power over time. This is why keeping everything in a savings account — while feeling “safe” — is actually a form of financial risk for long-term goals.

Category 05 — Investment Instruments

Ownership in a company. When you buy a share of stock, you become a part-owner — entitled to a proportional claim on the company’s assets, profits, and voting rights. Equities have historically delivered the highest long-term returns of any major asset class, alongside the highest short-term volatility.

A debt instrument through which an investor lends money to a company or government in exchange for periodic interest payments (coupon) and the return of principal at maturity. Bonds are generally lower risk than equities but also lower return. They provide stability and predictable income.

A pooled investment vehicle that collects money from many investors and deploys it into a portfolio of stocks, bonds, or other securities — managed by a professional fund manager. Mutual funds offer diversification, professional management, and accessibility with small amounts, making them ideal for beginners.

A fund that tracks an index, commodity, or basket of assets and trades on a stock exchange just like an individual stock. ETFs combine the diversification of mutual funds with the flexibility of real-time trading. They typically carry very low expense ratios, making them one of the most cost-efficient investment vehicles available.

The strategic decision of how to divide your investment capital across different asset classes — equities, bonds, gold, cash, real estate — based on your financial goals, time horizon, and risk appetite. Asset allocation is widely considered the single most important determinant of long-term portfolio performance, more influential than individual stock selection or market timing.

You Now Speak the Language of Investing

These 25 terms are not just definitions — they are the mental models that let you read a fund factsheet, understand a market news report, or have a meaningful conversation with a financial advisor without nodding politely while feeling lost.

The next step is not to memorise this list. It is to start applying these concepts to real decisions — beginning with the simplest ones: What is your goal? What is your time horizon? What is your risk appetite? The answers to those three questions will point you toward your first investment.

Remember: the best investment you can make today is in your own financial education. And you’ve just made a solid start.

- Understand the difference between assets and liabilities

- Know how compounding works — and start early

- Define your risk appetite before picking any instrument

- Use SIPs to build discipline without timing the market

- Diversify across asset classes, not just stocks

- Always invest with a time horizon in mind

- Learn to read CAGR before comparing any two investments

- Understand that volatility is not the same as loss