☀ Morning Brief

TUE · 02 JUNE 2026 · ISSUE #61

📉 GIFT Nifty: 23,264 · −197 pts · −0.84% · Gap-Down

·

🛢️ Brent: $95.04 · Bounced from $92.56 Low

·

🕊️ Iran MOU: Still Unsigned · Deal Delayed

·

🏦 FII Monday: −₹3,911 Cr · MSCI Rebalancing Hit

Morning Market Brief

Tuesday, 02 June 2026 · Issue #61

The Catch-Up That

Didn’t Come. GIFT Nifty

Falls Another 197 Points.

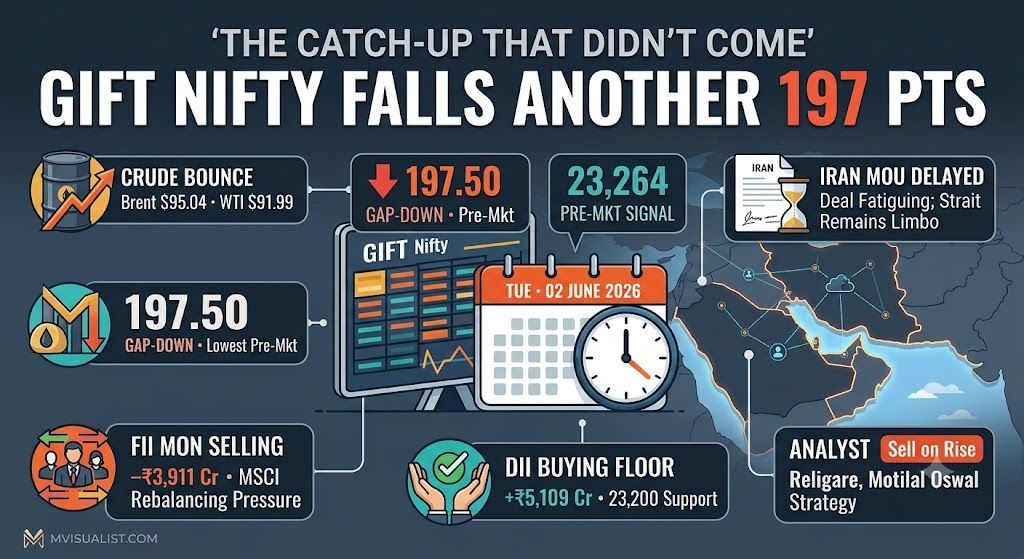

Monday’s hoped-for “India catch-up rally” ran into a wall of reality: FIIs sold ₹3,911 crore, crude bounced from $88.90 back to $95, the Iran MOU remained unsigned, and MSCI rebalancing triggered additional outflows. Tuesday opens with GIFT Nifty down 197 points at 23,264 — the lowest pre-market signal in weeks. Here’s your full Tuesday brief.

GIFT Nifty Gap-Down

−197.50

−0.84% · Lowest pre-mkt

FII Mon Selling

−₹3,911 Cr

MSCI outflows added

DII Mon Buying

+₹5,109 Cr

Preventing collapse

Brent Crude

$95.04

Bounced from $92.56

WTI Crude

$91.99

Back above $90

Iran MOU Status

Unsigned

Deal delayed

Analyst Stance

Sell on Rise

Religare, Motilal

Nifty Critical Floor

23,200–23,000

Today’s test

Monday June 1 — What Actually Happened vs What Was Expected

What Actually Happened (Bad)

• FII net sold ₹3,911.68 crore — no FII reversal

• MSCI rebalancing caused additional structural outflows

• Iran MOU still unsigned — deal delayed beyond weekend

• Crude bounced back: Brent $95 (from $92.56), WTI $92 (from $88.90)

• Nifty closed ~23,460 — no catch-up to global rally

• GIFT Nifty for Tuesday: −197 pts further gap-down

• MSCI rebalancing caused additional structural outflows

• Iran MOU still unsigned — deal delayed beyond weekend

• Crude bounced back: Brent $95 (from $92.56), WTI $92 (from $88.90)

• Nifty closed ~23,460 — no catch-up to global rally

• GIFT Nifty for Tuesday: −197 pts further gap-down

What Stayed Positive (Silver Linings)

• DII bought ₹5,109.13 crore — floor held

• Crude still significantly below May peak ($111.83)

• S&P 500 and Nasdaq remain near record highs

• Iran MOU “mostly agreed” — deal not collapsed, just delayed

• Midcap space shows stock-specific opportunities

• India VIX declined — fear easing gradually

• Crude still significantly below May peak ($111.83)

• S&P 500 and Nasdaq remain near record highs

• Iran MOU “mostly agreed” — deal not collapsed, just delayed

• Midcap space shows stock-specific opportunities

• India VIX declined — fear easing gradually

The Iran Deal Delay + MSCI Rebalancing + Crude Bounce: Three Compounding Headwinds on the Day India Needed Relief

Monday was supposed to be India’s catch-up session — pricing in Friday’s global rally on Iran MOU news and crude at $88.90. Instead, three compounding headwinds prevented any meaningful recovery. First: the Iran MOU remained unsigned over the weekend. Despite being “mostly agreed,” the deal that markets had been pricing in throughout the week failed to materialise as a formal announcement. This kept the “deal premium” in a frustrating limbo — too close to sell completely, too uncertain to buy aggressively. Second: MSCI rebalancing triggered structural FII outflows. The semi-annual MSCI index rebalancing, which adjusts country and stock weightings, caused mechanical FII selling in India that is independent of any fundamental view on the market — resulting in ₹3,911.68 crore in net FII outflows on Monday alone. Third: crude oil bounced. Brent recovered from its Friday low of $92.56 back to $95.04 — and WTI from $88.90 back to $91.99. This partial crude recovery, driven by Iran’s threat that “any ceasefire violation will be met with force” and continued uncertainty about Strait of Hormuz reopening timelines, erased some of the macro relief that had been building. For Tuesday, the combination of these three headwinds — delayed deal, MSCI outflows, and crude bounce — has pushed GIFT Nifty to a fresh gap-down of 197 points at 23,264. The critical question: can Nifty hold the 23,200–23,000 support zone that has been the market’s multi-week floor?

The Stories Behind Tuesday’s Open

Institutional · MSCI Rebalancing

MSCI Rebalancing Outflows Compounded FII Selling Last Week — Mechanical Pressure Now Largely Behind Us

The semi-annual MSCI index rebalancing — which typically occurs in late May — caused mechanical FII selling in Indian stocks that was independent of any fundamental investment decision. Global index-tracking funds that replicate MSCI Emerging Markets and MSCI India indices were forced to sell or buy stocks in proportion to their new weightings, which generated significant additional outflows from India last week and continued into Monday. Religare’s Ajit Mishra confirmed: “Investor sentiment remained under pressure due to persistent foreign institutional selling following the MSCI rebalancing-related outflows witnessed last week.” The critical insight for Tuesday: MSCI rebalancing is a one-time mechanical event, not a fundamental change in India’s investment attractiveness. With the rebalancing now largely complete, the structural FII selling pressure should ease — leaving only the Iran/crude macro headwinds as genuine fundamental drivers. This makes Tuesday’s selling more likely to be the last wave of technical outflows than the start of a new trend.

Geopolitics · Iran · Deal Fatigue Setting In

“Mostly Agreed” But Still Not Signed — Markets Beginning to Price in Deal-Delay Risk Premium

The Iran MOU that was “mostly agreed” as of Friday May 29 remains unsigned as Tuesday opens — creating a new phenomenon: deal fatigue. Markets have been pricing in an imminent Iran ceasefire deal for more than a week. Every day the deal doesn’t materialise, the “deal premium” (crude prices discounted from the $111.83 peak on the expectation of resolution) becomes more vulnerable to reversal. Brent crude bouncing from $92.56 (Friday) to $95.04 (Tuesday) reflects this deal-fatigue dynamic. BusinessToday’s morning note for Tuesday confirms: “Delayed deal between the US and Iran is also denting the sentiments further.” The White House disputed Iran’s stated MOU terms last week, with Trump saying “no nation will control shipping through the Strait” — while Iran insists the MOU must include US military withdrawal from the region. This terminological gap is what’s preventing signature. Watch for any Trump statement on Iran through Tuesday’s session — a positive signal would immediately push crude below $90 and trigger a 200–300-point Nifty intraday reversal.

Macro · Crude Oil · The Daily Variable

Brent at $95.04 — Up from Friday’s $92.56 Low, Still Well Below May’s $111.83 Peak

Crude oil’s partial recovery from Friday’s $92.56 (Brent) to Tuesday’s $95.04 reflects the market reassessing the Iran deal timeline. UBS noted that “there is still little evidence of any short-term improvement in vessel traffic or energy flows through the Strait of Hormuz” — meaning the actual physical supply situation hasn’t improved much despite diplomatic progress. Iran crude loadings remain below 0.3 million barrels per day (vs 1.7 mb/d pre-war). However, even at $95 Brent, the macro environment for India is dramatically better than the $111.83 May peak. The annualised import cost savings at $95 Brent vs $111.83 peak = approximately ₹10–12 lakh crore. The rupee remains firmer at approximately ₹95.40–₹95.60 vs the ₹96.14 record low. The key threshold: Brent staying below $100 keeps India’s macro in recovery mode. If crude re-spikes above $100, the rupee and FII narrative deteriorate rapidly.

Analyst Strategy · Sell on Rise

Both Religare and Motilal Oswal Recommend “Sell on Rise” — Midcap Stock-Picking Is the Week’s Playbook

Tuesday arrives with clear analyst consensus on the market approach. Ajit Mishra of Religare Broking: “We recommend the ‘sell-on-rise’ approach for the Nifty while continuing to focus on stock-specific opportunities based on sectoral trends, alongside disciplined risk and position management.” Siddhartha Khemka of Motilal Oswal: “Indian equities are expected to remain range-bound with a marginal negative bias in the near term amid persistent FII selling and ongoing uncertainty around global macro developments. Focus is likely to remain on stock-specific opportunities in the midcap space.” The implication is clear: the Nifty 50 benchmark is not the place to be in the immediate term. Midcap stocks with company-specific catalysts — earnings beats, order wins, management upgrades — are where alpha is being generated. The macro uncertainty makes large-cap index trading a low-conviction activity. Use dips in quality midcap names as accumulation opportunities; avoid chasing any Nifty 50 gap-ups as they are likely to be sold into.

Opportunity · Midcap Space

Midcap Space Outperforming — Nifty MidCap 100 Showed Resilience While Nifty 50 Sold Off

While the Nifty 50 has been under intense FII selling pressure, the Nifty MidCap 100 has demonstrated relative resilience — showing that domestic institutional money (DII buying ₹5,109 crore Monday) is being selectively deployed in quality mid-cap names rather than large-cap benchmark plays. This sector rotation reflects a key structural theme: midcap companies with strong domestic revenues are less affected by FII outflows (which are concentrated in large-cap Nifty stocks), less exposed to crude oil price swings, and generating earnings growth independent of the Iran/macro narrative. Motilal Oswal’s specific mention of “stock-specific opportunities in the midcap space” as the week’s focus confirms this as the institutional priority. Capital Goods, Pharma, Chemicals, and select FMCG midcaps are the sectors generating the most stock-specific interest in the current environment.

📌 “Sell on Rise” Framework — How to Navigate Tuesday’s Session

The Levels to Sell

23,550–23,600: First resistance on any bounce from gap-down. Sell Nifty futures/ETFs if rally reaches this zone.

23,700–23,750: 20-day EMA zone — strong resistance. Aggressive sell-on-rise target for Thursday close.

23,800+: Any close above this = buy, not sell. This is the bull confirmation level.

23,700–23,750: 20-day EMA zone — strong resistance. Aggressive sell-on-rise target for Thursday close.

23,800+: Any close above this = buy, not sell. This is the bull confirmation level.

The Levels to Buy

23,200–23,000: Multi-week critical support floor. DII buyers appear here. Quality names get accumulated at this zone.

22,900: Secondary support — extreme oversold zone.

Use gap-down opens in quality names as entry: Sun Pharma, TCS, HCL, HDFC Bank are the quality buys on weakness.

22,900: Secondary support — extreme oversold zone.

Use gap-down opens in quality names as entry: Sun Pharma, TCS, HCL, HDFC Bank are the quality buys on weakness.

What Changes the Narrative

Iran MOU signed: Immediately invalidates sell-on-rise. Buy aggressively on any crude drop below $88.

FII net buying for 3+ sessions: Structural reversal confirmed. Shift from sell-on-rise to buy-on-dip.

Brent above $100: Deepens sell-on-rise thesis toward 23,000 and below.

FII net buying for 3+ sessions: Structural reversal confirmed. Shift from sell-on-rise to buy-on-dip.

Brent above $100: Deepens sell-on-rise thesis toward 23,000 and below.

Stock-Specific Approach

Avoid large-cap index momentum trades. Focus on midcap earnings beats, order wins, capex cycle beneficiaries.

Best sectors for stock-picking: Capital Goods (L&T, ABB), Pharma (Sun, Cipla), Chemicals (Deepak Nitrite), FMCG (Tata Consumer).

Hold IT for US-India trade deal structural play.

Best sectors for stock-picking: Capital Goods (L&T, ABB), Pharma (Sun, Cipla), Chemicals (Deepak Nitrite), FMCG (Tata Consumer).

Hold IT for US-India trade deal structural play.

Tuesday’s Stocks to Watch

01

DefensiveDII Favourite

Sun Pharma / Cipla / Dr. Reddy’s — Defensive Anchor on Gap-Down

In a gap-down session with “sell on rise” as the market approach, pharma is the most compelling defensive position. Sector is unaffected by MSCI rebalancing selling (concentrated in large-cap indices), benefits from rupee at ₹95.40 (dollar revenue), and DII buyers specifically target pharma on weakness. Sun Pharma and Cipla are the two highest-conviction defensive accumulation names at gap-down prices.

02

Midcap FocusStock-Specific

Capital Goods — L&T / ABB India / Siemens (Midcap Layer)

Capital Goods was May’s outperforming sector rotation destination. L&T at the large-cap level; ABB India and Siemens in the midcap layer. India’s infrastructure capex cycle is insulated from Iran/crude macro. Government spending on roads, railways, and data centres continues irrespective of oil prices. The “stock-specific midcap” opportunity that Motilal Oswal identifies is most clearly visible here.

03

Iran Watch

IT Sector — TCS / HCL Tech (Hold; Add on Iran Deal)

IT holds its fundamental case (S&P 500 near records, Nasdaq at ATH, US-India 18% tariff deal) but faces FII selling pressure in the current environment. HCL Tech and TCS were among Monday’s relative outperformers. Hold existing positions; add aggressively only when Iran MOU is formally signed (crude falls → macro normalises → FII buying returns → IT re-rates). Don’t chase the sector on a gap-down day.

04

DII Support Zone

HDFC Bank / ICICI Bank — Buy at 23,200 Nifty Level

Private banks are the most rate-sensitive and FII-sold sector in the current environment. But DII buyers have consistently appeared at 23,200–23,000 Nifty levels with private bank accumulation. HDFC Bank and ICICI Bank, both trading at deep discounts to their pre-crisis valuations, are quality accumulation targets at gap-down prices. Use Tuesday’s weakness as accumulation, not panic selling.

05

Sell on Rise

Avoid Nifty Index Momentum Trades — “Sell on Rise” Is the Week’s Dominant Strategy

Both Religare and Motilal Oswal recommend “sell on rise” for the Nifty 50 index. Any gap-up attempt toward 23,600–23,700 should be used as a selling opportunity, not a buying trigger. The Iran deal delay, crude bounce, MSCI outflows, and persistent FII selling make the risk-reward unfavourable for long Nifty index trades this week. Capital preservation is Tuesday’s primary mandate.

“Indian benchmark indices are staring at a gap-down start on Tuesday on the back of cautious undertone as persistent geopolitical uncertainty continues to cloud investor sentiment. Elevated crude oil continues to add to the pressure on the Indian markets and currency. Delayed deal between the US and Iran is also denting the sentiments further. We recommend the ‘sell-on-rise’ approach for the Nifty while continuing to focus on stock-specific opportunities based on sectoral trends, alongside disciplined risk and position management.”

Ajit Mishra · SVP Research · Religare Broking · June 2, 2026

“Indian equities are expected to remain range-bound with a marginal negative bias in the near term amid persistent Foreign Institutional Investor selling and ongoing uncertainty around global macro developments. Investor sentiment remained under pressure due to persistent foreign institutional selling following the MSCI rebalancing-related outflows witnessed last week. Focus is likely to remain on stock-specific opportunities in the midcap space.”

Siddhartha Khemka · Head of Research · Motilal Oswal Financial Services · June 2, 2026

Tuesday’s Technical Levels

IndexKey Support (Buy Zone)Key Resistance (Sell Zone)

Nifty 50

23,200–23,000 → critical floor; DII buyers expected

22,900 → extreme oversold; secondary support

GIFT Nifty implies open near 23,264

22,900 → extreme oversold; secondary support

GIFT Nifty implies open near 23,264

23,500–23,550 → sell-on-rise zone 1

23,600–23,700 → sell-on-rise zone 2 (20-day EMA)

23,800+ → bull confirmation (buy only above this)

23,600–23,700 → sell-on-rise zone 2 (20-day EMA)

23,800+ → bull confirmation (buy only above this)

Sensex

73,400–73,600 → key support

73,000 → secondary support

73,000 → secondary support

74,500–75,000 → first resistance

75,800–76,000 → 20-day EMA resistance

75,800–76,000 → 20-day EMA resistance

Bank Nifty

52,000–51,500 → key support zone

50,000–49,500 → deeper support

50,000–49,500 → deeper support

53,500–54,000 → near resistance

54,400–55,000 → sell-on-rise target

54,400–55,000 → sell-on-rise target

Crude Watch

Brent $90–$92 = Iran deal optimism zone

Below $88 = formal MOU signed scenario

Below $88 = formal MOU signed scenario

Brent above $100 = macro crisis resumes

$95–$98 = current “deal fatigue” range

$95–$98 = current “deal fatigue” range

mvisualist · Tuesday Morning Verdict · Issue #61

Sell on Rise. Buy Quality on Dips. Wait for Iran.

Tuesday, June 2 opens as a session that demands discipline over emotion. GIFT Nifty at 23,264 (−197 points) means a gap-down open that immediately tests the 23,200–23,000 critical support floor. The reasons for caution are real and confirmed: FII sold ₹3,911 crore on Monday, crude bounced from $88.90 back to $95, Iran MOU remains unsigned, MSCI rebalancing added mechanical outflows, and India’s hoped-for catch-up rally failed to materialise. Both Religare and Motilal Oswal — two of India’s most credible market research houses — have explicitly recommended the “sell on rise” approach for the Nifty. Yet three structural positives keep the downside limited: DII bought ₹5,109 crore on Monday, absorbing more than the entire FII outflow; Iran MOU is delayed but not collapsed — “mostly agreed” means the deal is closer than ever; and crude at $95 is still dramatically better than the $111.83 May peak — India’s macro trajectory is positive even if the pace is slower than hoped. The week’s playbook: use gap-down opens to accumulate quality — Sun Pharma, TCS, HDFC Bank, Capital Goods — in the midcap and defensive segments. Sell any Nifty rally toward 23,600–23,700. Hold stops at 22,900 on large-caps. And keep the Iran news wire open — this market has one trigger that overrides all technical levels: the Iran MOU signature.

📉 GIFT −197 pts Gap-Down

🛢️ Brent $95 — Bounced

🕊️ Iran MOU Unsigned

📊 Sell on Rise: 23,600

🏦 DII Floor: 23,200

💊 Midcap = This Week’s Play

Key Events · Tuesday June 2

Pre-Mkt

GIFT Nifty 23,264 — check crude price and Iran news before session; both could override the gap-down Check First

9:15 AM

Gap-down open near 23,264–23,300 range; watch DII buying activation in first 15 minutes Opening

During

23,200 Nifty — critical DII support floor; if this holds, intraday recovery possible toward 23,450 Support Test

During

Iran news wire — any MOU signature by Trump = crude falls $5+ instantly = 200+ pt Nifty reversal. Most important intraday wildcard Iran Watch

During

Midcap stocks — focus on earnings winners, capex plays, pharma; avoid Nifty 50 index momentum trades Opportunity

If rally

Any bounce toward 23,550–23,600 is a sell-on-rise target per Religare and Motilal Oswal research

3:30 PM

FII/DII flow data — will post-MSCI FII selling ease today? A sub-₹2,000 Cr FII outflow = improvement signal FII Watch

FII / DII Flows · Monday June 1

FII — Net−₹3,911.68 Cr

DII — Net+₹5,109.13 Cr

FII driverMSCI rebalancing

FII YTD 2026~₹2.5L Cr out

Net combined+₹1,197 Cr

⚡ DII exceeded FII outflows on Monday — preventing a deeper selloff. Post-MSCI rebalancing, watch for FII selling to ease from Tuesday. A sub-₹2,000 Cr FII outflow today = meaningful improvement signal.

Commodities & Currency

Brent Crude (Tue)$95.04Bounced from $92.56

WTI Crude (Tue)$91.99Above $90 again

vs May Peak ($111.83)−$16.79Still −15% below

USD / INR~₹95.40Stable

Brent Bull threshold$100Macro crisis if above

Iran Loadings (May)<0.3 mb/dStrait still closed

JPM Q3 Forecast$104 avgPost-deal ceiling

Global Markets · Context

🇺🇸 S&P 5007,519.12 ★Near ATH

🇺🇸 Nasdaq26,656.18 ★ATH

Iran MOU“Mostly Agreed”Unsigned

MSCI RebalancingMostly doneEasing pressure

US 10Y Yield~4.6%Stable

RBI Dividend₹2.87L CrRecord · Positive

Tuesday’s Key Levels

GIFT Nifty23,264 (−197)

Sell-on-rise zone23,550–23,700

Bull confirmation23,800+ close

DII support floor23,200–23,000

Next support22,900

Bank Nifty support52,000–51,500

Key catalystIran MOU sign