☀ Morning Brief

WED · 03 JUNE 2026 · ISSUE #62

⚡ GIFT Nifty: +76 pts · +0.33% · Positive Open

·

💻 Nifty IT Surge: +4.23% Tue · Infosys +5.68%

·

🏆 Dow Jones: 51,032 · NEW All-Time Record

·

📅 Wipro Buyback: Record Date June 5

Morning Market Brief

Wednesday, 03 June 2026 · Issue #62

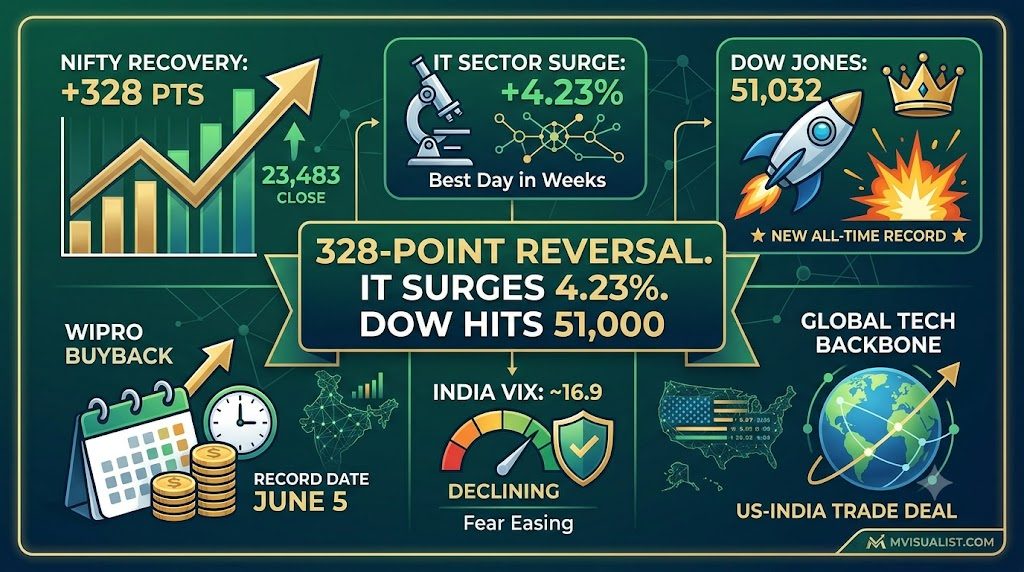

328-Point Reversal.

IT Surges 4.23%.

Dow Hits 51,000.

Tuesday delivered the market’s most impressive intraday recovery of June — Nifty opened at 23,229 and clawed back 328 points to close at 23,483. Infosys surged 5.68%. The Dow Jones hit a fresh all-time record of 51,032. GIFT Nifty opens Wednesday at +76 points. The cautiously bullish narrative is building. Here is everything before 9:15 AM.

Tue Nifty Reversal

+328 pts

From 23,229 low

Nifty IT (Tue)

+4.23%

Best day in weeks

Infosys (Tue)

+5.68%

₹1,270.80

Dow Jones

51,032 ★

Record! +0.72%

Nasdaq

26,972

Near 27,000

India VIX (Tue)

~16.9

Declining · Fear easing

Wipro Buyback

June 5

Record date Friday

Bullish Candle

Reversal

Tue pattern strong

Tuesday June 2 — The Session That Changed the Week

+4.23%

Nifty IT

31,116 · Session’s engine

+5.68%

Infosys

₹1,270.80 · Top Nifty gainer

+2.03%

DLF

Real estate recovery

+2.02%

Adani Enterprises

Momentum continues

+1.66%

Wipro

Buyback June 5 catalyst

−2.98%

NTPC

Power sector weak

Infosys +5.68%. Nifty IT +4.23%. The Technology Sector Did What the Whole Market Needed.

Tuesday’s session was the market’s most impressive recovery of the young June 2026 month. Nifty opened at a harsh 23,229 gap-down — immediately testing the critical 23,200 support floor. But then something remarkable happened: the Nifty IT sector launched a 4.23% rally that single-handedly arrested the broader market’s decline and pulled the benchmark index from its 23,229 open all the way to a 23,556 intraday high and a 23,483 close. Infosys led the charge with a stunning 5.68% gain to ₹1,270.80 — its best single-day performance in months. The recovery of 328 points from the day’s low to close is technically described as a “bullish reversal candle” — a pattern that signals the downtrend from the recent high (24,089 on May 26) has found meaningful support at 23,200–23,229. The structural driver of the IT rally is clear: the Dow Jones closed Tuesday at 51,032 — a new all-time record (+0.72%) — and the Nasdaq closed at 26,972 (+0.21%). US technology strength, the US-India 18% tariff deal, and deeply oversold RSI levels in Indian IT stocks created the perfect setup for a snap-back. The Sensex closed at 74,649.84 (+0.52%) and India VIX fell to approximately 16.9 — its lowest since the May crisis began.

The Stories Shaping Wednesday

💻 Nifty IT’s 4.23% Surge — Tuesday’s Top Performers

Infosys

+5.68%

₹1,270.80 · Session leader · US-India deal

Wipro

+1.66%

Buyback record date June 5 catalyst

Nifty IT Index

+4.23%

31,116.55 · Best single day in weeks

HCL Tech / TCS

↑ Positive

IT sector broad-based buying

Sector · IT — The Week’s Recovery Engine

IT’s 4.23% Rally Was Driven by Three Structural Catalysts — Can Day 2 Continue?

Tuesday’s Nifty IT surge to +4.23% was not a random bounce — three structural catalysts converged to create it. First: the Dow Jones at 51,032 (new record) and Nasdaq at 26,972 create the strongest US technology backdrop of 2026. When the Dow hits new all-time highs, global institutional investors reassess their emerging market IT exposure. Second: the US-India 18% tariff deal continues to be progressively priced into IT stocks’ earnings outlook — improving the medium-term margin and revenue trajectory for US-revenue IT companies. Third: deeply oversold technical levels — the Nifty IT index had fallen over 26% YTD before the recent recovery, and at RSI levels below 30, mean reversion moves of 4–6% in a single session are technically expected. For Wednesday, the question is continuation. Univest’s Ankit Jaiswal predicts the IT rally will be the dominant theme Wednesday, with the sector looking to build on Tuesday’s momentum. Infosys, HCL Tech, and TCS are the primary names to watch for Day 2 of the recovery.

Global · Dow 51,032 — Another Record

Dow Jones Hits Fresh All-Time High at 51,032 Tuesday — The Third Record Close in Two Weeks

The Dow Jones Industrial Average closed at a new all-time record of 51,032.46 (+0.72%) on Tuesday June 1 (US time) — its third record close in the past two weeks. The Nasdaq closed at 26,972.62 (+0.21%) — within touching distance of the 27,000 milestone. Wall Street’s record-setting run reflects markets pricing in a benign macro scenario: Iran deal imminent (crude at $92–$95, well below the $111.83 peak), US economy resilient, AI-driven technology earnings robust, and the Fed’s hawkish stance gradually becoming less restrictive. For Indian markets, every Dow record is a positive signal — it removes the “risk-off rotation to US safety” motivation that had been driving FII outflows from India. With the Dow above 51,000 and the Nasdaq approaching 27,000, the fundamental case for FII return to Indian equities is stronger than at any point in 2026.

Corporate Event · Wipro Buyback

Wipro Buyback Record Date June 5 — A Specific Catalyst Creating Weekly Momentum

Wipro has a share buyback record date of Friday, June 5, 2026 — meaning shareholders who hold Wipro shares at the close of trading on June 5 will be eligible to tender shares in the buyback. This creates a predictable intraday pattern through this week: buyers accumulating Wipro shares to qualify for the buyback premium, driving the stock progressively higher. Wipro gained +1.66% on Tuesday and is likely to continue its trajectory as June 5 approaches. The buyback premium (the price at which Wipro buys back shares, typically above market) represents a guaranteed return for qualifying shareholders, making accumulation ahead of the record date a defined-risk trade. Wipro is therefore a specific, calendar-driven opportunity this week independent of the broader Iran/macro narrative — a rare anchor of certainty in an otherwise volatile market.

Institutional Flows — The Most Encouraging Weekly Data

FII Selling Fell from ₹21,105 Crore (May 29 MSCI Day) to ₹3,911 Crore (June 1) — Structural Moderation

The most encouraging institutional data of the week arrived in Tuesday’s session context: FII net selling moderated sharply from ₹21,105.86 crore on May 29 (MSCI rebalancing day) to ₹3,911.68 crore on June 1 — an 81% reduction in selling intensity in a single session. This confirms that the extreme May 29 outflow was primarily mechanical MSCI-rebalancing-related selling rather than fundamental conviction selling. With the MSCI rebalancing now largely complete, Tuesday’s session saw FII selling continuing to ease while DII bought ₹5,109.13 crore. If Wednesday’s FII selling falls below ₹2,000 crore, it would represent the most significant structural improvement in institutional flows since the May crisis began. Three consecutive sessions of sub-₹2,000 crore FII selling would be the clearest signal yet that the June 2026 FII narrative is turning from “persistent selling” to “selective return.”

Geopolitics · Iran · Background Risk

Iran Deal Still in “Mostly Agreed” Limbo — But Crude Staying Below $96 Signals Market Patience

The Iran MOU remains unsigned despite being “mostly agreed” — creating a peculiar market situation where the primary risk catalyst is well-known, partially priced, but unresolved. Brent crude holding in the $92–$96 range (vs the $111.83 peak) confirms that oil markets still believe the deal will eventually be signed — they haven’t significantly reversed the crisis-peak pricing. For Wednesday’s session, the Iran narrative is secondary to the IT momentum and Dow record — but it remains the week’s wild card. Any Trump announcement on Iran during Wednesday’s session would immediately dominate all sector narratives. A positive signal (MOU signed) → crude below $88 → gap-up across auto, aviation, OMCs, banks, and real estate. A negative signal (ceasefire collapse) → crude above $100 → full risk-off reversal of Tuesday’s gains. Keep one eye on the news wire through Wednesday’s session.

Wednesday’s Stocks to Watch

01

Day 2 ContinuationIT Leader

Infosys / HCL Tech / TCS — IT Rally Day 2

Infosys’s 5.68% Tuesday surge puts it at ₹1,270.80. With Dow at 51,032, Nasdaq approaching 27,000, and the US-India trade deal as structural support, Day 2 of the IT recovery is the highest-conviction Wednesday trade. HCL Tech (strongest mid-market US exposure) and TCS (Nasdaq tracker) should continue. Watch for any sector profit-booking above Nifty IT 31,500 — that would be a healthy pause, not a reversal signal.

02

Buyback Record June 5

Wipro — Accumulate Before Record Date

Wipro’s share buyback record date is Friday June 5. Three trading days remain. The buyback premium above current market price creates defined-return buying pressure. Wipro +1.66% Tuesday was pre-buyback accumulation in action. Wednesday and Thursday should see continued buying. Use any intraday dip as an entry opportunity — the June 5 record date is a hard calendar catalyst.

03

Real Estate Revival

DLF — RE Sector Leading the Recovery

DLF gained +2.03% on Tuesday — the real estate sector’s best single-day performance since the May rout. As crude eases and inflation trajectory improves, the rate-cut narrative gradually revives, which is directly positive for real estate. DLF is the bellwether for the broader RE recovery trade. Its continued Tuesday gains signal institutional confidence in the rate-outlook improvement even before a formal rate cut announcement.

04

Accumulate on Dip

HDFC Bank / ICICI Bank — Quality at Discount

Despite Axis Bank (-1.94%) and ICICI Bank (-1.06%) declining Tuesday, private banks at current levels represent deep discount to pre-crisis valuations. HDFC Bank and ICICI Bank’s fundamental case — RBI no off-cycle hike, improving macro, US-India trade deal — is intact. Wednesday’s GIFT Nifty +76 signal should provide a mild lift. Use any gap-up weakness in banks as quality accumulation opportunity with a 3–6 week view.

05

Defensive Hold

Sun Pharma / Cipla — Maintain Defensive Allocation

Even on a recovery Wednesday, pharma remains the portfolio’s defensive anchor. India VIX declining to ~16.9 is positive but doesn’t warrant abandoning defensive positions. Sun Pharma and Cipla continue to benefit from rupee at ₹95 (dollar exports), strong domestic healthcare demand, and US-India trade deal. Hold through the current recovery as the portfolio’s risk ballast.

06

Avoid

NTPC / REC / Power Sector — Sector-Specific Weakness

NTPC (-2.98%) and REC (-1.92%) were Tuesday’s biggest losers — continuing a multi-session trend of power-sector underperformance. Regulatory uncertainty, rising interest rate expectations (from hot WPI), and FII selling targeting rate-sensitive power-infrastructure names make this sector the one to avoid in the current environment. No near-term catalyst visible for reversal.

“The stock market predictions for tomorrow 3 June 2026 are cautiously bullish after Indian equity markets staged a powerful intraday recovery on 2 June 2026. Nifty 50 opened sharply lower at 23,229.15 on GIFT Nifty weakness, but recovered 328 points off the session low to close at 23,483.55 (+0.43%), finishing above the June 1 closing level of 23,382.6. The defining story was Nifty IT surging 4.23 per cent to 31,116.55, led by Infosys which gained +5.68% to Rs 1,270.80. Stock market predictions for tomorrow are shaped by this decisive IT-led bounce, a significant moderation in FII selling, and the Wipro buyback record date approaching on June 5.”

Ankit Jaiswal & Kunal Singla · Univest Research · June 2, 2026

“Positive Start Expected: With Gift Nifty trading 0.52% higher and domestic benchmarks ending the previous session in the green, Indian markets are likely to see a firm opening on Wednesday, supported by improving risk appetite.”

5paisa Research · Key Cues Ahead of June 3 Trade

Wednesday’s Technical Levels

IndexKey Support ZonesResistance / Targets

Nifty 50

23,350 → June 2 intraday support (Univest)

23,232 → 5paisa technical level

23,200–23,000 → critical multi-week floor

23,232 → 5paisa technical level

23,200–23,000 → critical multi-week floor

23,480–23,550 → Choice India resistance band

23,700–23,750 → 20-day EMA · recovery confirm zone

23,800+ → bull case if momentum extends

23,700–23,750 → 20-day EMA · recovery confirm zone

23,800+ → bull case if momentum extends

Sensex

73,800–74,000 → key support

73,614 → next support level

73,614 → next support level

75,000–75,200 → immediate resistance

75,800–76,000 → 20-day EMA zone

75,800–76,000 → 20-day EMA zone

Nifty IT

30,500–30,800 → post-rally support

Tuesday’s +4.23% creates new floor at 30,500

Tuesday’s +4.23% creates new floor at 30,500

31,500–32,000 → Day 2 bull target

Dow 51,032 + Nasdaq 26,972 = structural support

Dow 51,032 + Nasdaq 26,972 = structural support

India VIX

~16.9 (declining) · Below 18 = fear easing significantly

Below 15 = structural bull signal confirmed

Above 20 = Iran escalation risk returned

Above 20 = Iran escalation risk returned

mvisualist · Wednesday Morning Verdict · Issue #62

The Recovery Is Building. IT Is Leading It. Wednesday Confirms or Tests.

Wednesday, June 3 arrives as the most constructive morning since the May 25 “Dow 50,000 / Nifty 24,031” session. Tuesday’s 328-point Nifty intraday recovery — driven entirely by an extraordinary 4.23% IT sector rally and Infosys’s 5.68% single-day surge — created the most technically significant bullish reversal candle of June. The Dow Jones hit 51,032 (another record). India VIX fell to ~16.9. FII selling moderated 81% from May 29’s MSCI-rebalancing peak. GIFT Nifty signals a +76 point positive open. These are not isolated data points — they are a consistent pattern of improving momentum. The caveat: Tuesday’s close of 23,483 is still 548 points below the May 25 peak of 24,031. The “sell on rise” thesis from Religare doesn’t disappear after one good session. Iran MOU remains unsigned. The 23,480–23,550 zone (Choice India’s resistance band) will face genuine supply. Wednesday’s playbook: ride the IT momentum for Day 2 — Infosys, HCL Tech, TCS. Accumulate Wipro before the June 5 buyback record date. Hold DLF for the real estate revival narrative. Watch the 23,550 level — a clean close above this on Wednesday would shift the technical narrative from “bear rally” to “recovery rally” and open the path to 23,800.

💻 IT +4.23% Day 2 — Key Watch

🏆 Dow 51,032 New Record

⚡ GIFT +76 pts Positive

📅 Wipro Buyback June 5

📉 VIX 16.9 — Fear Easing

🎯 Watch: 23,550 Close

Key Events · Wednesday June 3

Pre-Mkt

GIFT Nifty +76 pts (~23,560) — positive open; IT momentum continuation expected Watch

9:15 AM

IT sector open — Infosys Day 2 after +5.68%; Wipro pre-buyback accumulation; Nifty IT targets 31,500+ IT Focus

During

23,550 Nifty test — Choice India resistance zone; a clean close above this = bear rally becomes recovery rally Level Test

During

Wipro accumulation — June 5 buyback record date is 2 sessions away; buying momentum should persist today Buyback

During

Iran news wire — any MOU progress = crude drops, 300+ pt rally. Any escalation = reversal Iran Watch

During

India VIX direction — hold below 18 = fear easing confirmed; spike above 20 = Iran risk resurgence signal VIX Watch

3:30 PM

FII/DII flows — will selling stay below ₹2,000 Cr? A third consecutive session of sub-₹4,000 Cr FII selling = structural improvement Flow Data

Tuesday’s Close — Context

Nifty 5023,483.55+0.43%

Sensex74,649.84+0.52%

Bank Nifty53,714.65+0.13%

Nifty IT31,116.55+4.23%

Infosys₹1,270.80+5.68%

DLF—+2.03%

Adani Enterprises—+2.02%

India VIX~16.9Declining

NTPC—−2.98%

Axis Bank—−1.94%

Global Markets · Tuesday Close

🇺🇸 Dow Jones51,032 ★+0.72% Record!

🇺🇸 Nasdaq26,972+0.21% Near 27K

Iran MOU“Mostly Agreed”Still unsigned

Brent Crude~$95Stable range

WTI Crude~$92Holding below $95

USD/INR~₹95.40Stable

FII June 1−₹3,911 Crvs ₹21,105 May 29

Wednesday’s Key Levels

GIFT Nifty~23,560 (+76)

Nifty resistance23,480–23,550

Nifty bull target23,700–23,800

Nifty support 123,350

Nifty support 223,232

Nifty critical floor23,200–23,000

Wipro record dateFriday June 5

India VIX targetBelow 15